TAX & COMPLIANCE | MARCH 2026 | By IPPC Group (I.P. Pasricha & Co) | Chartered Accountants | Member firm of Russell Bedford International | March 27, 2026

Financial Year End Checklist 2026 India: Three days. That is all that stands between you and the end of FY 2025–26. In our experience working with businesses across India, most year-end problems are not caused by ignorance – they are caused by assuming someone else is handling it. This guide covers every compliance task your business must close, file, or decide before the year ends.

Why This Year-End Is Different From Any Other

Every March has its deadlines. But March 2026 is a hinge point for Indian businesses. The new Income Tax Act 2025 comes into force on April 1, 2026, and with it, the default tax regime changes permanently. The deductions most businesses and individuals have relied on for years – Section 80C investments, HRA claims, home loan interest, health insurance premiums under 80D – will not automatically apply from next year unless you actively opt out of the new regime.

This means FY 2025–26 is your last full year to extract maximum value from the old framework. For a business owner or director with Rs.1.5 lakh in 80C investments, an HRA claim, and a home loan, the difference in tax outgo between regimes can easily be Rs.60,000 to Rs.1.5 lakh or more. The window to make that choice closes at midnight on March 31.

“We have seen clients lose six-figure deductions simply because they assumed their CA would take care of it. Your CA can execute – but the decisions are yours to make, and they have to be made before the deadline.”

The Complete 15-Task Checklist

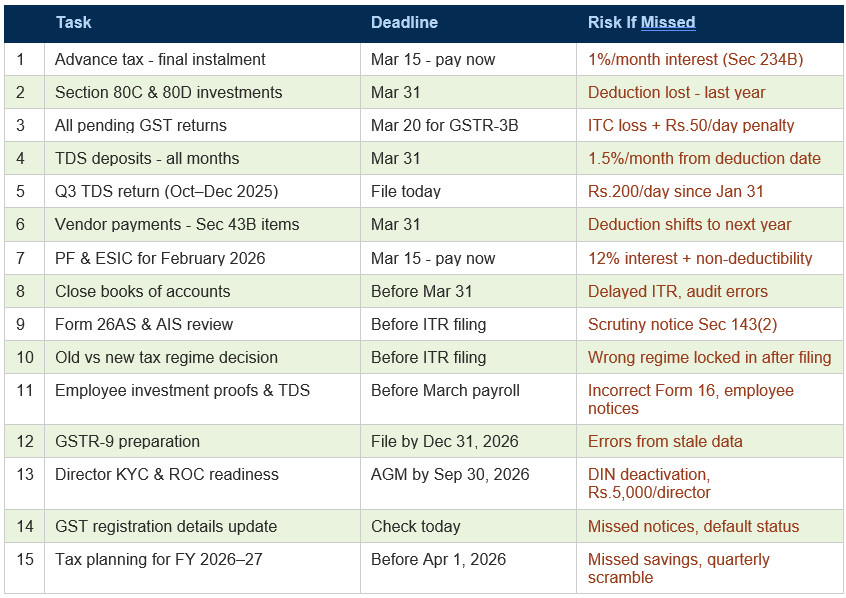

1. Pay Your Final Advance Tax Instalment – If You Have Not Already

⏰ Was due: March 15 – pay immediately if pending

The fourth advance tax instalment was technically due on March 15. If you missed it, the interest clock under Section 234B has already started – 1% per month on the shortfall, running from April 1. Paying now still limits the damage. What you must not do is wait until July when you file your ITR, because the interest will have compounded across three months by then.

IPPC Tip: Calculate your full-year income, subtract TDS already deducted by clients or banks, and pay the balance now. Do not estimate conservatively – underestimating and paying less also attracts Section 234C interest.

2. Make Your 80C and 80D Investments Today – Not “This Week”

⏰ Hard deadline: March 31, 2026

The Rs.1.5 lakh Section 80C deduction limit exists for this year. Next year, under the new default regime, it will not reduce your taxable income unless you opt out. An ELSS fund investment made today counts for FY 2025–26. Waiting until March 30 is fine technically, but payment processing delays on the last day are real. If you have Rs.50,000 or Rs.1 lakh still unused under 80C, invest it today.

IPPC Tip: Also check 80D – health insurance premiums paid this year for yourself, spouse, children, or parents qualify for up to Rs.25,000 (Rs.50,000 for senior citizens). This benefit also disappears under the new default regime.

3. Reconcile and File Every Pending GST Return

⏰ GSTR-3B for February due: March 20

Pull up your GST dashboard and check every month from April 2025 to February 2026. One unfiled GSTR-1 or GSTR-3B does not just attract a Rs.50-per-day penalty – it breaks your Input Tax Credit chain for that month. ITC blocked due to a filing gap cannot be claimed retroactively once the September 2026 return window closes. That is a real cost, not just a compliance checkbox.

IPPC Tip: After filing returns, run a GSTR-2B reconciliation against your purchase register. Vendor invoices that appear in your books but not in 2B are a red flag the department will act on during scrutiny.

4. Deposit Every Rupee of Pending TDS

⏰ Deadline: March 31 (April 7 for March deductions)

TDS deducted from salaries, professional fees, rent, and contractor payments during the year must be deposited in full. Outstanding TDS from months prior to March attracts 1.5% interest per month from the date it was deducted – not from when you remember. The AIS system cross-references every payment, and gaps surface automatically.

IPPC Tip: If you deducted TDS but forgot to deposit for even one month – say, August 2025 – the interest has already been running for seven months. Pay it now and stop the meter before it hits another month-end.

5. File Your Q3 TDS Return If It Is Still Pending

⏰ File immediately – every day adds Rs.200

The Q3 TDS return covering October to December 2025 had a January 31 due date. If it is sitting unfiled, Section 234E is charging Rs.200 per day from that date. At the time of writing this, that is already 55 days – Rs.11,000 in late fees before you open the portal. File it today. While you are at it, compile Q4 data (January to March) so that return is ready to go by May 31.

6. Pay Outstanding Professional Fees, Loan Interest, and Bonuses

⏰ Hard deadline: March 31, 2026

Section 43B of the Income Tax Act is one of the most misunderstood provisions in small business accounting. Certain categories of expenses – professional fees, bank loan interest, employee bonuses, PF contributions – are only allowable as deductions in the year they are actually paid, not when they are accrued in the books. If your books show an outstanding professional fee of Rs.2 lakh that you intend to pay in April, that Rs.2 lakh remains taxable income this year. Pay it before March 31 and save the tax now.

7. Deposit PF and ESIC Contributions for February

⏰ Due: March 15 – pay now if pending

Provident Fund contributions for February 2026 were due by March 15. ESIC contributions follow the same timeline. Beyond the 12% per annum interest on delayed PF, unpaid PF contributions also fall under the Section 43B problem – they are not deductible until actually paid. Two reasons to clear this immediately: tax deductibility this year, and avoiding enforcement action from EPFO.

8. Close Your Books of Accounts – Do Not Wait for Your CA to Ask

⏰ Target: before March 31

The most common thing we hear in July is: “I will send you the statements, just give me a few days.” Those few days stretch to weeks because the books were never closed in March. Closing your books now means reconciling every bank account to the last rupee, writing off or resolving all suspense account entries, booking every outstanding expense that belongs to this year, and locking down your closing stock with a physical verification.

IPPC Tip: A business that hands its CA closed, reconciled books in April files its ITR in June. A business that hands over a mess files in September – often with errors, sometimes with penalties.

9. Download and Review Your Form 26AS and AIS

⏰ Do this before filing your ITR

The Annual Information Statement on the Income Tax portal contains a remarkable amount of information about your business: TDS deducted by clients and banks, large purchases and sales, mutual fund transactions, property deals, and your GST-reported turnover. If your books show Rs.80 lakh in revenue but your AIS shows Rs.95 lakh in transactions, that mismatch will generate a notice under Section 143(2). Identify discrepancies now, explain them in your records, and your ITR filing becomes straightforward.

10. Run the Old vs New Tax Regime Calculation for Your Specific Numbers

⏰ Decision must be made before filing ITR

Generic advice on which regime to choose is useless – the answer depends entirely on your income level, the deductions you actually claimed this year, and your business structure. A salaried director with a home loan and 80C investments often does better under the old regime. A business owner with high turnover and lower personal deductions may find the new regime cleaner. Run your actual numbers with your CA. Once you file your ITR, the decision is locked.

IPPC Tip: Contact us at IPPC Group for a quick regime comparison calculation. It takes less than 30 minutes with complete data and can save you significant money.

11. Collect All Employee Investment Proofs and Finalise March TDS

⏰ Before processing March salary

March payroll is the last chance to correct TDS deducted on employee salaries for the entire year. Ask every employee to submit their final investment proofs – LIC premium receipts, PPF contribution slips, rent receipts for HRA, home loan interest certificates. If you over-deducted TDS during the year, refund the excess through the March salary. If you under-deducted, recover the balance. Getting this wrong means your employees receive incorrect Form 16s and face tax demand notices.

12. Prepare GSTR-9 While the Year’s Data Is Still Fresh

⏰ File by December 31, 2026 – but start now

GSTR-9, the annual GST return, is mandatory for businesses above Rs.2 crore in turnover. The filing deadline is December 31 of the following year, which makes it easy to defer. Do not. Preparing GSTR-9 in March – when you have access to every invoice, every reconciliation statement, and every GSTR-2B – takes hours. Preparing it in November from nine-month-old records takes days, and the errors that creep in are expensive to correct after filing.

13. Check Director KYC and ROC Status for Your Private Limited Company

⏰ AGM due by September 30 – start paperwork now

If you run a Pvt Ltd company, the AGM for FY 2024–25 must happen before September 30, 2026. But the financial statements needed for that AGM – audited accounts, directors’ report, auditor’s report – take weeks to prepare. Starting in March rather than August is the difference between a smooth AGM and a last-minute scramble. Also verify DIR-3 KYC for every director. A non-compliant DIN gets deactivated and you cannot sign board resolutions or filings until it is restored. Penalty: Rs.5,000 per director.

14. Verify Your GST Registration Details Are Current

⏰ Check today

Log into your GST portal and confirm that your registered business address, authorised signatory details, and linked bank account are correct. Every GST notice, refund, and assessment communication goes to the address on record. If you moved offices or changed your signatory during the year and did not update the portal, notices may have already been issued – and timelines for responding may have begun without your knowledge.

IPPC Tip: If your turnover crossed Rs.40 lakh this year and you are still operating without GST registration, that is a default that needs to be corrected immediately, not in April.

15. Use the Next Four Days to Plan FY 2026–27 – Not Just Close FY 2025–26

⏰ Before April 1, 2026

Most business owners spend March closing the old year. The ones who come out ahead spend part of March designing the new one. Before April 1: decide your tax regime for FY 2026–27, restructure your salary if the new regime changes what makes sense, review whether your business is in the right legal form (proprietorship, LLP, or Pvt Ltd), and set your Q1 advance tax target so June 15 does not sneak up on you. One planning session now is worth four reactive conversations with your CA later in the year.

| Important Note on March 31 Falling Near a Weekend When March 31 falls on a non-working day, some deadlines shift to the next working day – but not all. Investments for tax deductions such as 80C must reflect in the system by March 31 regardless. Do not rely on a deadline extension that may not apply to your specific task. |

Quick Reference: All 15 Tasks at a Glance

Frequently Asked Questions

I run a small business with under Rs.50 lakh turnover. Does all of this apply to me?

Most of it does. Advance tax, Section 80C investments, TDS obligations, and the old vs new regime decision apply regardless of business size. GSTR-9 and statutory audit are more relevant above Rs.2 crore and Rs.1 crore respectively, but books closure and GST reconciliation are universal. If you are unsure which items apply to your specific business, get in touch – we can walk you through it in a single call.

We missed several of these deadlines. Is it too late to do anything?

It is rarely too late – but delay always costs more. Most penalties accrue daily or monthly, so the sooner you act, the less you pay. Some things, like the 80C deduction for this year, are genuinely unrecoverable after March 31. But TDS deposits, GST returns, and advance tax can all be filed late with interest. The goal now is to stop the meter and start the clean-up.

Should I choose the old or new tax regime for FY 2025–26?

There is no universal answer. The old regime favours taxpayers with significant deductions – home loans, 80C investments, HRA, NPS. The new regime is simpler and works better for those without many deductions. For business income, the new regime allows all legitimate business expenses but removes personal investment deductions. We recommend running the actual numbers with a CA rather than using any general rule of thumb.

Can IPPC Group help with any of these tasks before March 31?

Yes. We are available this week for year-end reviews covering advance tax calculation, GST reconciliation and return filing, TDS compliance, books closure, 26AS and AIS analysis, and tax regime comparison. We work with businesses across India. Reach us at sailfreely(Replace this parenthesis with the @ sign)capasricha.com or visit www.ippcgroup.com to schedule a call.

| IPPC Group | I.P. Pasricha & Co Chartered Accountants | Member firm of Russell Bedford International Our team is conducting free year-end compliance reviews for businesses this week. Let us go through your specific situation before March 31. 🌐 www.ippcgroup.com ✉ sailfreely(Replace this parenthesis with the @ sign)capasricha.com |

IPPC Group · I.P. Pasricha & Co · Chartered Accountants · Member firm of Russell Bedford International